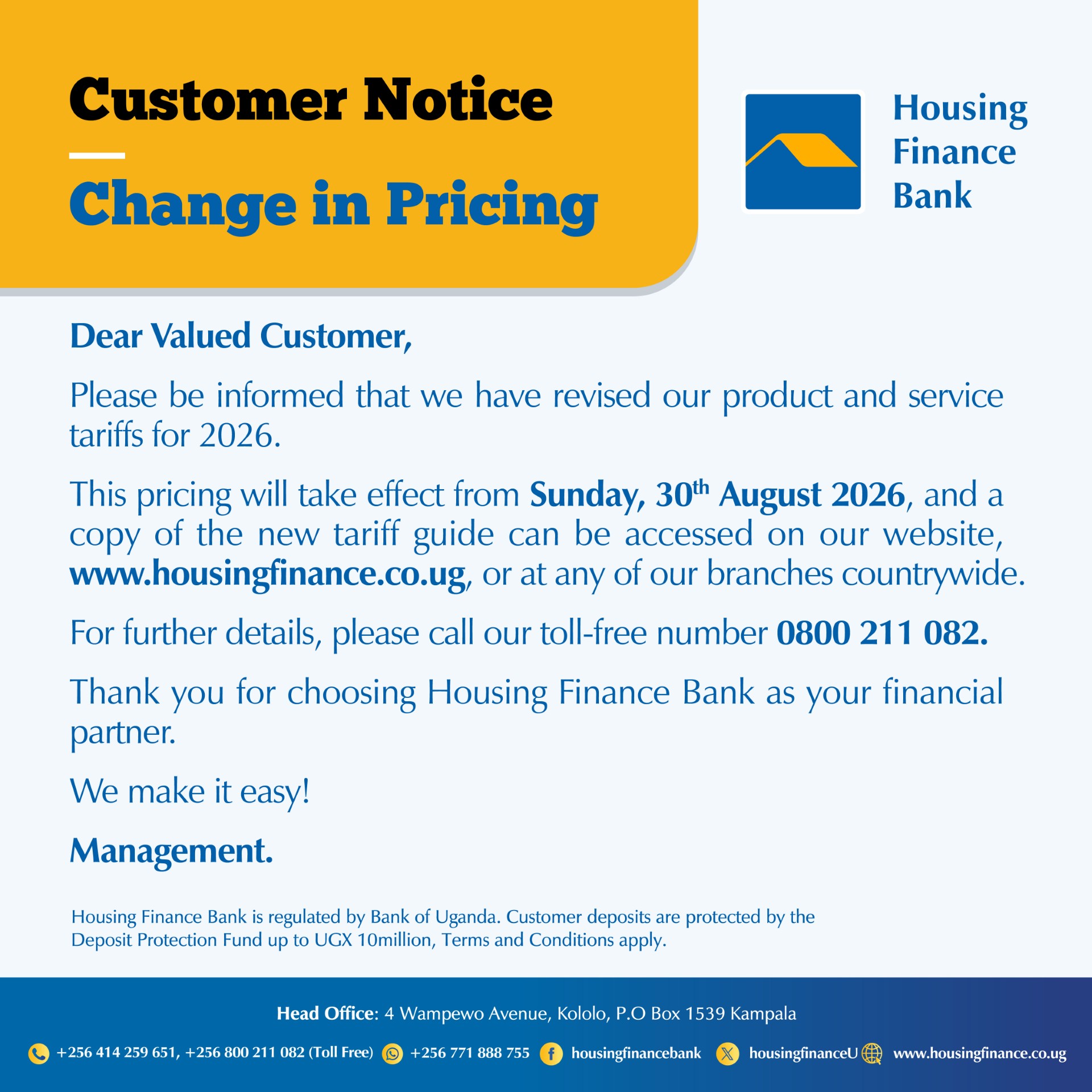

This Insurance Policy provides financial protection against loss or damage to property caused by fire and allied perils such as lightning, explosion, riots, strikes, malicious damage, storm, flood, and impact by vehicles or aircraft.

2. Who can take a Fire Insurance Policy?

Any individual, company, or institution that owns or has an insurable interest in property such as:

- Buildings (residential, commercial, or industrial)

- Plant, machinery, and equipment

- Furniture, fittings, and stock

- Office contents, computers, and documents

3. What does a Fire Policy cover?

- Fire, lightning, or explosion

- Riot, strike, or malicious damage

- Storm, flood, or wind damage

Earthquake, volcanic eruption, or subterranean fire - Impact by vehicles, aircraft, or objects falling therefrom

- Overflow or leakage from water tanks or sprinklers

4. What is not covered under the policy?

- War, invasion, or civil commotion

- Nuclear risks or radioactive contamination

- Intentional acts or gross negligence by the insured

- Consequential loss (e.g. loss of profit) unless specifically insured under a Business Interruption Policy

- Electrical faults not leading to fire (e.g. short circuits damaging wiring only)

5. What are the key features of a Fire Insurance Policy?

- Sum Insured: The maximum amount payable in case of loss.

- Premium Rate: Usually 0.125% but, Determined by the type of property, location, risk exposure, and safety measures in place.

- Policy Period: Usually 12 months, renewable annually.

- Excess/Deductible: The amount the insured bears per claim.

- Average Clause: If the property is underinsured, the insurer pays proportionately to the sum insured.

6. What documents are required to buy a Fire Policy?

• Completed Proposal Form

• Valuation or estimate of property to be insured

• Proof of ownership (e.g. title, invoice, or lease)

• Company registration documents (for businesses)

• National ID or TIN (for individuals)

7. How do I file a claim in case of fire?

- Notify the bank immediately by contacting your RM, at the branch or through email at [email protected] or contact us on 0417803000 0r 0200803000 for support

- Call the fire brigade and police and secure the affected property.

- Complete the insurer’s Claim Form and submit all required documents.

- Provide the Fire Brigade and Police Reports.

- Allow inspection by the insurer’s loss assessor/adjuster.

- Await assessment, settlement offer, and payment once a discharge voucher is

signed.

8. What documents are required when lodging a fire claim?

- Completed Claim Form

- Copy of the policy and proof of premium payment

- Fire Brigade Report and Police Report (where applicable)

- Inventory of damaged items

- Proof of ownership and value (receipts, invoices)

- Photos of damage

- Repair estimates or contractor quotations

- Bank details for payment

9. How long does it take to settle a fire claim?

- The bank should acknowledge your claim within 3 working days.

- Loss assessor should be appointed within 5 working days.

- Settlement or repudiation should be made within 5 working days after final report.

- Payment should be made within 10–20 working days after you sign the discharge voucher (depending on claim amount).

10. How is compensation determined?

- The extent of damage (partial or total loss)

- The value of property insured

- The sum insured in your policy

- The average clause (if underinsurance applies)

- The deductible/excess stated in the policy

11. Can I extend my Fire Policy to cover more risks?

Yes. Fire policies can be extended to include:

- Burglary and Theft

- Explosion only policy

- Public Liability (for third-party damage)

- Sprinkler leakage

- Earthquake or Terrorism extensions (on request)

Always request for a copy of your Insurance Certificate at any Housing Finance Bank branch or by emailing us at [email protected] or contact us on 0417803000 0r 0200803000 for support.

Housing Finance bank Bancassurance is regulated by the insurance regulatory Authority of Uganda.

Enjoy quick and flexible banking with our Mobile Banking App

With only a few taps, get all your financial needs fulfilled through the HFB mobile app. It brings you convenient, fast, and secure banking on the go.